Summary: This article discusses the IRS’s increasing focus on cryptocurrency tax enforcement. It highlights that the IRS is stepping up its efforts to identify and prosecute taxpayers who fail to report cryptocurrency transactions or pay the required taxes. This article emphasizes that cryptocurrency is considered property for tax purposes, and transactions are subject to capital gains taxes. It advises taxpayers to keep accurate records of all cryptocurrency transactions and report them on their tax returns. Failing to comply with cryptocurrency tax laws can result in penalties and legal consequences.

With the value of Bitcoin passing $20,000 in 2020, the interest in cryptocurrency is at an all-time high. As cryptocurrencies continue to gain popularity among investors, the IRS has needed to rework how it regulates the virtual market. To assist the IRS with this monumental task, the U.S. Department of Justice (DOJ) released a detailed Cryptocurrency Enforcement Framework.

If you’re interested in cryptocurrency or already own some virtual assets, you need to be aware of what this new Cryptocurrency Enforcement Framework entails. Below, you’ll learn the illicit uses of cryptocurrencies, the enforcement actions of the IRS and how to comply with cryptocurrency laws and regulations.

The Cryptocurrency Enforcement Framework released by the DOJ goes over the potential threats caused by cryptocurrency, cryptocurrency laws and regulations and the challenges of regulating cryptocurrency. Below, you’ll learn what cryptocurrency uses are illegal and how the IRS limits the illicit use of cryptocurrency.

IRS Commissioner Chuck Rettig has moved to increase criminal investigations, meaning taxpayers could be investigated for things such as tax evasion. To avoid a criminal investigation, taxpayers must know what qualifies as the illegal use of cryptocurrency. The DOJ’s Framework outlines the general categories of illicit cryptocurrency uses.

Illicit uses of cryptocurrency usually fall under one of the following three categories:

The IRS is looking to take more action against taxpayers who fail to report their cryptocurrency transactions. The IRS believes that millions of transactions using cryptocurrency are not being reported, despite growing awareness regarding tax rules for cryptocurrency. The IRS considers cryptocurrency a form of property and taxpayers are required to report it correctly on their tax returns and pay the necessary taxes. Taxpayers who fail to do so can face penalties or even criminal investigations.

However, due to the decentralized nature of cryptocurrency, it can be challenging to regulate. As governing bodies adapt and strategize about the best ways to regulate cryptocurrency, the IRS has become stricter about how taxpayers report cryptocurrencies. Specifically, the Bank Secrecy Act (BSA) and the Anti Money Laundering (AML) laws serve as the primary tools of enforcement. These laws ensure that ownership is taken of all cryptocurrency assets, including nonconventional virtual asset exchanges like peer-to-peer transfers.

To increase cryptocurrency regulation, the IRS sent around 10,000 letters to taxpayers who had dealt with cryptocurrency last year, and the new 1040 for 2019 contained a question regarding cryptocurrency. A checkbox on the form requires taxpayers to answer whether they sold, sent, exchanged, or acquired a financial interest in cryptocurrency. The IRS added the checkbox to help improve compliance from taxpayers and to remind them to report their cryptocurrency transactions. Failure to check that box can carry high penalties and an increased chance of criminal investigation.

These tighter rules and regulations have resulted in more cryptocurrency investigations. In fact, the IRS has seized $1.2 billion worth of cryptocurrency during the 2021 fiscal year. For those uncertain how to properly account for cryptocurrency when filing taxes, reaching out to a tax attorney to review any cryptocurrency records can help them avoid a criminal investigation.

The IRS has stated that cryptocurrency is a property for tax purposes. That means you pay taxes on it if you had any type of gain from it and you can also claim losses if you suffered one from the cryptocurrency. You will need to know how much you paid for the currency and what you received for it.

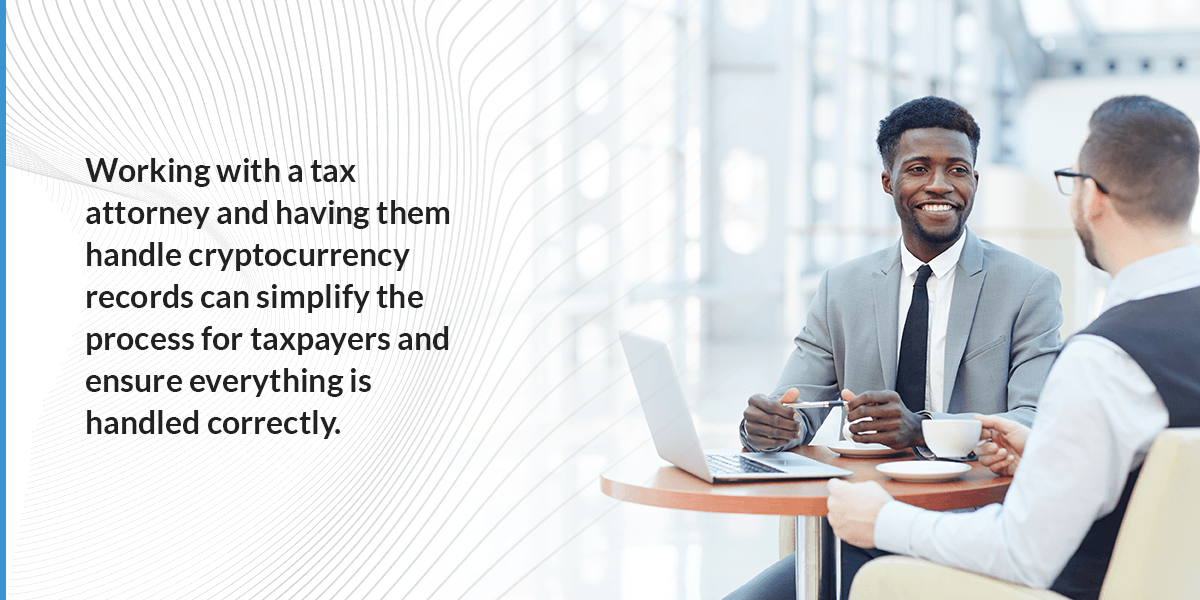

The IRS has published a list of FAQs on its website to help answer taxpayers’ questions regarding cryptocurrency. The FAQs particularly emphasize that taxpayers are required to maintain excellent records to establish positions taken on tax returns. Taxpayers should keep and maintain their records documenting all their receipts, their sales or exchanges, or other dispositions of virtual currency and the fair market value of the virtual currency. Working with a tax attorney and having them handle cryptocurrency records can simplify the process for taxpayers and ensure everything is handled correctly.

If you’re uncertain how to handle your cryptocurrency during tax season, Polston Tax Resolution & Accounting can help. At Polston Tax, we offer cryptocurrency services to help you file your property taxes correctly and avoid a cryptocurrency investigation by the IRS. We will also review your cryptocurrency compliance obligations and ensure that any deficiencies get resolved quickly.

For more information about how Polston Tax can help you comply with cryptocurrency regulations, contact us today.