The evolving and growing cannabis industry offers businesses the opportunity for growth. With frequently changing federal and state regulations, you may be concerned about compliance issues and unsure which business expense deductions you can claim for your cannabis company. Fortunately, you don’t have to face the challenges of running a cannabis business alone.

Whether you own a startup or an established dispensary, knowledgeable, experienced accountants can customize accounting services to meet your exact business needs. To further guide you through business expense deductions, we cover information like Section 280E, who in the cannabis industry pays taxes, what you can and can’t deduct and how to protect your business against audits.

Under the Controlled Substances Act, marijuana was labeled a Schedule I controlled substance alongside drugs like ecstasy, heroin and LSD. During the height of drug hysteria and higher incarceration rates related to drug charges, Congress established Section 280E in 1982.

This section of the Internal Revenue Code (IRC) was created after a court case involving a convicted methamphetamine, marijuana and cocaine trafficker. The trafficker filed a tax return and claimed that the current federal tax law gave him the right to deduct ordinary business expenses, including advertising, rent and employee salaries. At the time, the dealer was permitted to take these deductions.

280E was created to prevent drug dealers from claiming these deductions for ordinary and necessary business expenses when trafficking controlled substances. Under IRC 61, all income is taxable, including income from businesses that are considered illegal by federal law.

Today, legal cannabis businesses must operate in compliance with regulations regarding access to adult-use cannabis and medical marijuana and pay taxes for ordinary business expenses. On your taxes, you must distinguish between non-trafficking and trafficking expenses.

Section 280E is an IRS tax code that is intended to stop taxpayers from claiming deductible expenses related to the sales of marijuana, amphetamines and cocaine. No individual or business can claim tax deductions related to running a business or trade that involves trafficking controlled substances. Before 280E was passed, deductible tax expenses included costs related to transportation, shipping, packaging and weighing these substances.

For your cannabis business, the following are the effects of IRS code 280E:

Despite the recent legalization of cannabis and its increased medical use, cannabis remains a Schedule I controlled substance. This means tax accounting can get confusing with new state laws and federal income taxes. Technically, there are no write-offs for a cannabis business owner. Now that multiple states allow a form of legal marijuana, Section 280E applies to state-regulated cannabis businesses more frequently than the illegal drug dealers the code was intended to penalize.

From the outside, it can seem like cannabis businesses are swimming in profits, but Section 280E can mean a large portion of your revenue is lost to taxes. This tax liability could hinder your business from being able to roll out raises, invest in building improvements, pay benefits and cover operational expansions.

Until the classification of marijuana changes at the federal level, you must abide by 280E if you want to operate a cannabis business. To avoid growing pains and struggling with tax requirements, reach out to a tax professional to learn how you can be proactive about your business responsibilities.

Yes, Section 280E applies to growers, along with other medical marijuana business types that involve touching the plant and its products in the supply chain. Marijuana verticals that Section 280E may affect include:

The tax impact for a cannabis cultivator is typically less severe than that on a cannabis dispensary. This is because cannabis retailers are involved more directly with selling cannabis, while growers have more costs associated with producing cannabis products and not conducting transactions.

Even if your cannabis business is operating in a legal recreational or medical state, Section 280E still applies to your business, as trafficking cannabis is still in violation of current federal law. Though any business that involves touching cannabis should adhere to 280E tax laws, some exceptions may apply that can reduce a business’s total tax liability.

Yes, dispensaries and other marijuana businesses must file and pay federal taxes. Your business may also be taxed at the state level, so it’s essential to understand the tax rules and how they may affect your business. States may set taxes based on the weight, potency or sale price of the substance. You will also need to file and pay federal income tax on your business’s sales each year.

On a state level, your tax obligations vary depending on the location of your dispensary. In states where marijuana has been legalized, you will face a sales tax requirement, and in some, you will also pay an excise tax — taxes businesses pay on specific goods. The following are some of your tax obligations by state:

The cannabis sector is growing quickly and is now a multi-billion dollar industry. As state laws regarding cannabis have been changing and these businesses have recently become legal, regulations can be confusing. In terms of taxation, state laws vary. One of the greatest challenges for cannabis business owners is the significantly higher tax rate compared to other businesses. Luckily, there are a couple of exceptions to Section 280E.

In a federal tax court case known as Californians Helping to Alleviate Medical Problems, Inc. (CHAMP) v. Commissioner, it was ruled that Section 280E doesn’t prohibit taxpayers from claiming the cost of goods sold, or COGS.

COGS are expenses that are necessary to extract, construct or acquire a physical product to be sold. CHAMP argued they should be permitted to deduct operating expenses related to production, along with services offered to the community that did not involve plant-touching. CHAMP won its case, and the case has set a precedent for other businesses to deduct costs from other departments.

With this exception, your business can reduce its total tax liability, especially if your cost of goods sold is significant. This Section 280E exception could mean the best way to maximize your business profits is by assigning indirect and direct costs to inventory.

The key is understanding what you can deduct and what you cannot. You should work with a cannabis accountant to carefully analyze what you can deduct while staying compliant. Some of the 280E deductible labor COGS your business may be able to deduct can include:

For example, this exception means growers may be able to deduct expenses associated with labor, electricity and seeds — essentially, anything that directly goes into growing and preparing the cannabis for sale. If you own a stand-alone dispensary, your COGS may be limited to the costs of the product and acquiring the merchandise, which can include the transportation costs for buying the wholesale cannabis.

If you’re still unsure what you can deduct under this exception, turn to tax attorneys and Certified Public Accountants (CPAs) for assistance.

Some states exclude the 280E tax code in calculations for state income tax, such as Oregon and Colorado. As a result, your licensed cannabis business can deduct each standard business expense. If you operate a cannabis business in one of these states, your income tax burden can be significantly reduced. Bookkeeping and accounting may be a bit more complex, but it’s nothing that professionals can’t handle.

As a marijuana business owner, you can deduct the cost of goods sold. This deduction is essentially the cost of your inventory. Fortunately, there are a number of expenses that you can claim as COGS.

For a cultivation team, labor costs are deductible, such as trimming, cultivating, processing and harvesting. The employee benefits for the production team are also considered tax-deductible, assuming the cannabis business produces financial statements that adhere to the Generally Accepted Accounting Principles (GAAP).

Your direct and indirect costs related to production processes may be deductible. Below, we break down direct costs and indirect costs and examples of each.

Direct costs for production are necessary for your business’s production operations. Direct material costs refer to materials that are consumed during production or become an essential part of the product. Direct labor costs include compensation, overtime pay, sick leave pay, payroll taxes, holiday pay and vacation pay.

Examples of direct costs that you may be able to deduct include:

Indirect costs for production can be capitalized to ending inventory as well. Indirect costs cannot be attached to specific items produced. During the production process, indirect costs are known as manufacturing overhead. The more COGS you are able to assign to inventory, the less income tax your cannabis business may owe. Examples of indirect costs that you may be able to deduct include:

If your cannabis business is involved solely in growing and selling marijuana wholesale, the majority of your expenses are often tax-deductible. If your operation develops a brand to sell or distribute directly to dispensaries, taxes can get more complicated, and costs associated with sales, marketing and distribution may be subject to 280E.

Work with an accountant who can identify what percentage of your rent or electricity is deductible. You can deduct only the expenses that are related to your designated inventory area. For example, the rent for your facility may be deductible, but only the portion in which the cannabis is stored. You will subtract your break rooms, bathrooms and offices to arrive at the correct amount allowable for the deduction. To learn more about dispensary tax deductions, speak with a tax preparer who’s knowledgeable about the cannabis industry.

Though the cost of goods sold can be deducted under Section 280E, there are several expenses that your cannabis business cannot deduct on your tax return. These costs can include:

Typically, salaries of executive, marketing or sales positions aren’t assigned to COGS. To maximize deductions, identify overlap between your employees’ different activities. While a CEO may not be spending a lot of time working with these plants, for example, a portion of their salary could be deductible under Section 280E. Additionally, some delivery costs are considered tax deductible, while others aren’t. If you’re unsure whether your marijuana distribution and transportation costs are deductible or not, reach out to a tax professional for further guidance.

Since taxpayers can claim the medical expense deduction in some cases, the question of whether you can deduct medical marijuana on your taxes naturally comes up. Medical bills can add up quickly, and being able to claim a deduction can save you money at tax time.

Though medical marijuana may be legal in several states, it is not considered tax deductible by the IRS. Because cannabis is still illegal at the federal level, the IRS claims not to have discretionary authority regarding policies permitting marijuana-related tax deductions. As a marijuana business owner, stick with what you know you can deduct, such as your cost of goods sold.

Though some states offer tax guidance to businesses selling cannabis, it’s essential to remain compliant with both federal and state taxes as applicable. Cannabis businesses tend to deal mostly in cash, as they may not be able to use traditional banks for depositing earnings. This setup can create unique challenges for both cannabis businesses and the IRS when it comes to promoting tax compliance.

IRS audits are always a possibility. Among cannabis businesses, dispensaries tend to be the subject of IRS audits. The IRS can audit your tax returns and documentation from many past years, and you could be penalized if you owe back taxes. As such, getting your taxes right from the beginning is crucial. Follow the steps below to protect your business against audits.

You can create a corporate structure for your cannabis business that limits your liability. For a cannabis business, you may deal with high income tax liability, so maximizing potential tax deductions on your gross income should be a top priority. Typically, C-corporations are recommended for businesses in the marijuana industry opposed to LLCs. However, before you determine which structure is right for your business, consult with a CPA to determine which is the best option for your cannabis company.

To protect your cannabis business against audits, ensure you obtain the proper licensing according to the requirements in your location. States and regulatory agencies strictly regulate cannabis businesses. Familiarize yourself with the licensing requirements in your state.

If you have stakeholders investing in your cannabis business, ensure your investors are contributing positively to your company.

The federal designation and social stigma associated with an illegal substance have led to unregistered financing, and when there are beneficial owners, this can lead to complex compliance challenges. This is because beneficial owners enjoy the benefits of owning a business, but the title or activity of the property is in someone else’s name. Compliance issues that could occur include failing to accurately report gross receipts or file a tax return. IRS agents will review these arrangements closely.

Be wary of investors who may attempt to use funds for nefarious reasons. For example, an investor may put in a few thousand dollars that lead your business to become complicit in laundering money, which means converting money that has been gained illegally to “clean” or legitimate money. Through the payments you make to the IRS, the government is likely able to trace this laundered money, which could lead to compliance and legal issues for your business. Examples of money-laundering behaviors to avoid include:

Money-laundering violations can lead to investigations, civil litigation, loss of your cannabis license or jail time.

Many cannabis businesses do not use a bank to store their funds and instead conduct their transactions in cash. This setup is due to marijuana still being classified as a Schedule I controlled drug in the U.S.

If your cannabis business receives an amount greater than $10,000 in cash in transactions within a 12-month period, you need to file Form 8300. On this form, you will report this cash payment. You must file this form within 15 days after you receive the payment, so it’s essential to be diligent about this reporting requirement.

You must file and pay your taxes on time, even if your cannabis business operates solely with cash. Since the Internal Revenue Code, or IRC, does not distinguish between legal and illegal sources of income, you must report all your income on your tax return, even if paid entirely in cash. If your cannabis business uses cryptocurrency, be aware that the IRS considers this to be property, and the gains are taxable.

Partner with an experienced CPA who can help you reduce your gross receipts and accurately calculate your cost of goods sold to determine your cannabis company’s gross income. Like other small businesses, cannabis businesses are often required to make quarterly tax payments. Whether you are a grower, wholesaler, transporter or retailer, be sure to pay your taxes on time to avoid accruing interest or penalties.

When managing 280E deductions, accurate record keeping can save your cannabis business hours and spare you from making costly mistakes. One of the best ways to set your cannabis business up for success is by preparing a strong chart of accounts with your accountant. By doing so, maintaining good records will be simple, as you have already determined the direct, indirect and non-deductible expenses.

Keep records of the documents that support a source of income or expense, such as receipts and canceled checks. Even if an expense isn’t deductible, keep records of it, as this will make it easier to complete your tax returns, substantiate items you report on your returns and provide answers if your business is audited. Ensure you have an electronic method to manage your documentation and report every cash transaction, including:

Record each employee’s job description in detail and review these descriptions regularly, in the event that an employee’s responsibilities change. How an employee spends time at work can determine whether a medical marijuana business is able to deduct the costs as COGS or whether the activity is non-deductible.

Similarly, you should also keep detailed records of each employee’s labor time. You can use this to prove the amount of the employee’s labor time that is tax deductible. You can use time-tracking software to keep your detailed records of employees’ labor hours. Select software that is built specifically for cannabis entrepreneurs, complete with time-tracking and task management features and common cultivation activities like harvesting, transplanting, feeding and cloning.

Software that offers accurate tracking features can help you identify 280E deductions and reduce the impact of 280E on your business. Software specifically designed for cannabis businesses to track employee time provides:

Software specifically designed for cannabis businesses can handle the many tax intricacies and complex regulatory environment of the marijuana industry. With proper understanding and management, you can prevent Section 280E from eroding your profits or impacting your cannabis business excessively.

The cannabis industry is unique and can make it challenging to prepare your taxes. To successfully operate a licensed cannabis business, work with a professional in accounting and tax law, like the team at Polston Tax.

We can help you understand your tax obligations and avoid penalties. We have extensive experience within the cannabis industry, and we can analyze your expenses and assign them to ordinary business expenses or COGS. We can help you designate specific COGS and guide you on how to record detailed COGS deductions, along with discerning what qualifies and what doesn’t.

This understanding will help set your business up for success and offer you the peace of mind needed to ensure your business is in compliance with the law while you’re simultaneously deducting as much as you can on your tax return. When you can utilize 280E best practices and authenticate COGS, expenses and labor hours, you may be able to offset unnecessary tax payments. We can also help your cannabis business avoid behaviors related to money laundering, which can be especially common for all-cash businesses.

When your partner with Polston Tax, we can help protect your business from audits by:

Even if you take all the possible steps to avoid an audit, IRS audits are particularly common for cannabis businesses. Fortunately, by establishing clear accounting processes with a trusted tax attorney like Polston Tax, you can ensure your business is prepared to successfully get through an audit.

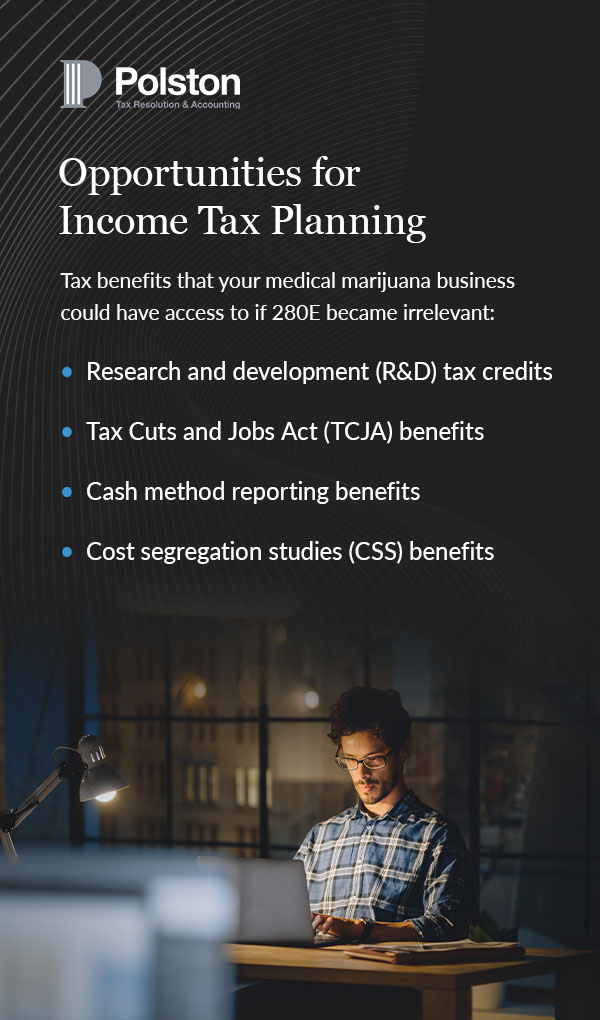

The legalization of cannabis could affect the future of 280E. If Section 280E becomes irrelevant due to legalization at the national level, cannabis businesses could have access to opportunities for income tax planning.

As of 2022, 37 states and the District of Columbia have approved the medical use of cannabis. Nineteen states and the District of Columbia have approved measures intended to regulate cannabis for non-medical use for adults. Some of the states where recreational marijuana is currently legal include:

Some states like Colorado, California and Washington offer tax guidance for cannabis businesses. Though there are still states that prohibit cannabis use, both licensed and unlicensed marijuana businesses are expected to grow, and more states are expected to legalize cannabis. Additionally, the rise in state-level cannabis legalization may eventually lead to legalization on the federal level.

If cannabis is one day no longer classified as a controlled substance, Section 280E would no longer apply to cannabis businesses, although new legislative proposals could affect marijuana taxes. For example, medical marijuana excise taxes could be imposed on products made in the U.S., or an occupational tax may be imposed on marijuana manufacturing and cultivation facilities.

If Section 280E becomes irrelevant for marijuana businesses based on the legalization of cannabis, your business may have access to opportunities for income tax planning that are currently not available to you. The following are some of the tax benefits that your medical marijuana business could have access to if 280E became irrelevant:

If, someday, cannabis is legalized on a national level or Section 280E is considered moot for another reason, cannabis businesses could greatly benefit from these opportunities for income tax planning and saving.

At Polston Tax, we offer cannabis CPA accounting and tax services to help you navigate cannabis tax laws and overcome regulatory hurdles. We are committed to providing your business with accurate, powerful accounting solutions to help you remain compliant. Our services are designed to assist your cannabis business in achieving your objectives. Some of the cannabis accounting services we can offer your business include:

We can help you allocate costs so your business can optimize its deductions and potentially reduce the taxes you owe. Contact us at Polston Tax or call 844-841-9857 to schedule a free consultation.