A bank levy often occurs after significant financial delinquencies and signals the critical need for immediate action or resolution. Receiving a legacy notice can be distressing, but you can handle it efficiently with professional guidance and a timely response.

Understanding how bank levies work can help you address your payments proactively before they escalate into disruptive financial consequences.

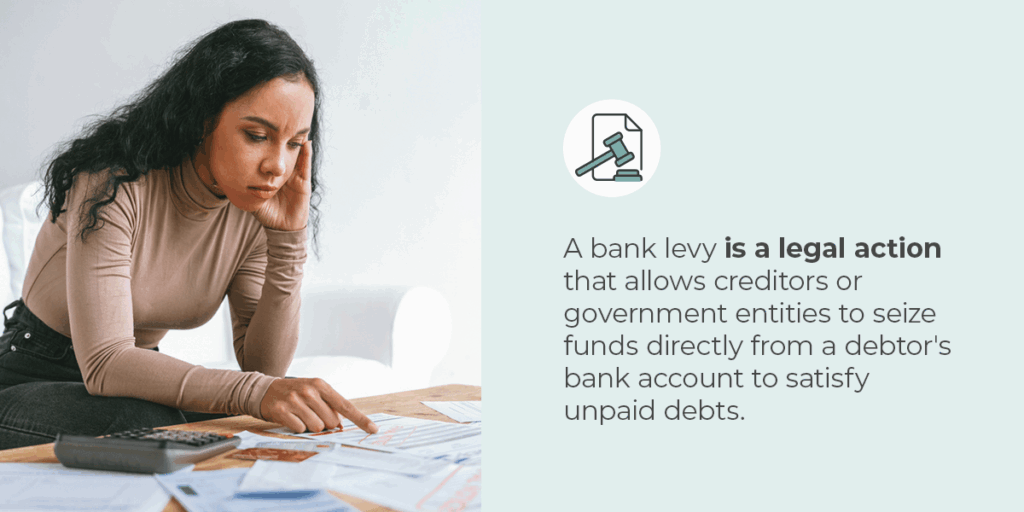

A bank levy is a legal action that allows creditors or government entities to seize funds directly from a debtor’s bank account to satisfy unpaid debts. It often occurs after a court judgment or due to statutory authority, such as unpaid taxes. Bank levies are typically a last-resort measure, signaling significant financial distress or the account holder’s noncompliance. Types of bank levies include:

When a levy is placed, the bank freezes the account, restricting access to funds until the debt is resolved. It can halt critical personal or business transactions, causing financial strain, particularly for businesses that may struggle to meet payroll or cover operational costs.

Debit orders from these accounts can incur insufficient funds fees or penalties, which can damage credit scores. In some cases, multiple levies or unresolved debts can lead to bankruptcy or additional legal actions.

A bank levy is triggered by a creditor or government agency, often after obtaining legal authority. It may involve a court judgment for private debts or statutory power for an issue like unpaid taxes. The creditor sends a levy notice or garnishment order to the debtor’s bank. At this stage, the debtor is usually notified of the impending action, though the levy may be executed quickly, leaving you 21 days to respond.

The IRS can levy your bank account as a one-time effect, taking an asset at once. If you fail to respond to the notices, any future levies must undergo the same notification process before seizing assets.

When the bank receives the levy notice, it freezes the account, preventing the account holder from accessing funds. After the freeze period, the bank releases the levied funds to the creditor or government agency. The payment satisfies part or all of the debt, depending on the balance in the account and the amount owed.

Any remaining debt may result in further collection actions, such as additional levies or wage garnishments, until the creditor is fully reimbursed.

Receiving a bank levy notice can be financially and emotionally overwhelming, but proactive and strategic action can help minimize its impact.

A prompt response to receiving this notice is essential. Start with the following steps:

Facing a bank levy can be daunting, but there are legal pathways to protect your rights and finances. While you can attempt some of these strategies yourself, partnering with tax professionals can ensure the best outcome:

Bank levies can severely disrupt business operations, jeopardizing cash flow, vendor relationships and employee payroll. Businesses must adopt proactive measures to safeguard their financial health and prevent levies from recurring to avoid such consequences.

Ensure all income, expenses and liabilities are documented to provide a clear financial picture. This transparency creates opportunities for identity and early addressing of potential debt issues. It is also essential to stay updated with tax filing and payments. Hiring tax professionals can help minimize errors and avoid penalties that can lead to levies.

Develop a structured plan to address outstanding debts, focusing on high-priority obligations like secured loans and government dues. Where necessary, work with creditors to renegotiate payment plans, interest rates or settlement amounts to manage liabilities. Finally, build a contingency fund to cover unexpected expenses or delinquent accounts to ensure you can meet critical obligations without falling into arrears.

Address lawsuits, judgments or any tax liens on your property promptly to prevent them from escalating into bank levies. Seek mediation or settlement options before these disputes reach the enforcement stage. It is also essential to keep track of credit scores and address any negative marks that can increase the likelihood of creditors taking legal action. Regular risk assessments of outstanding liabilities, cash reserves, financial health and risk exposure help you identify vulnerabilities and take corrective action before issues escalate.

Bank levies are a clear signal of financial mismanagement or unresolved disputes. Addressing these issues proactively is essential to avoid the severe repercussions that accompany this measure. By maintaining strong financial practices, prioritizing debt and partnering with reputable tax professionals, businesses and individuals can reduce the chances of future bank levies and foster long-term stability.

Since 2001, Polston Tax Resolution and Accounting has helped various organizations and individuals navigate bank levies. Our team of knowledgeable and experienced tax attorneys will work tirelessly to help. We will provide you with advice to mitigate future bank levies, help you eliminate penalties and interest and give you peace of mind, knowing that you have professionals on your side.

Contact us for your free consultation and get relief today.