If you’re a business owner, knowing when and how to write off meals and entertainment when you file your taxes can be tricky. While some items aren’t deductible, others are 50% deductible or 100% deductible. Whether a meal or event is deductible and by how much depends on its purpose and who it benefits. To help you save on your return, we’ll walk you through the deductions for meals and entertainment your business can take this tax season.

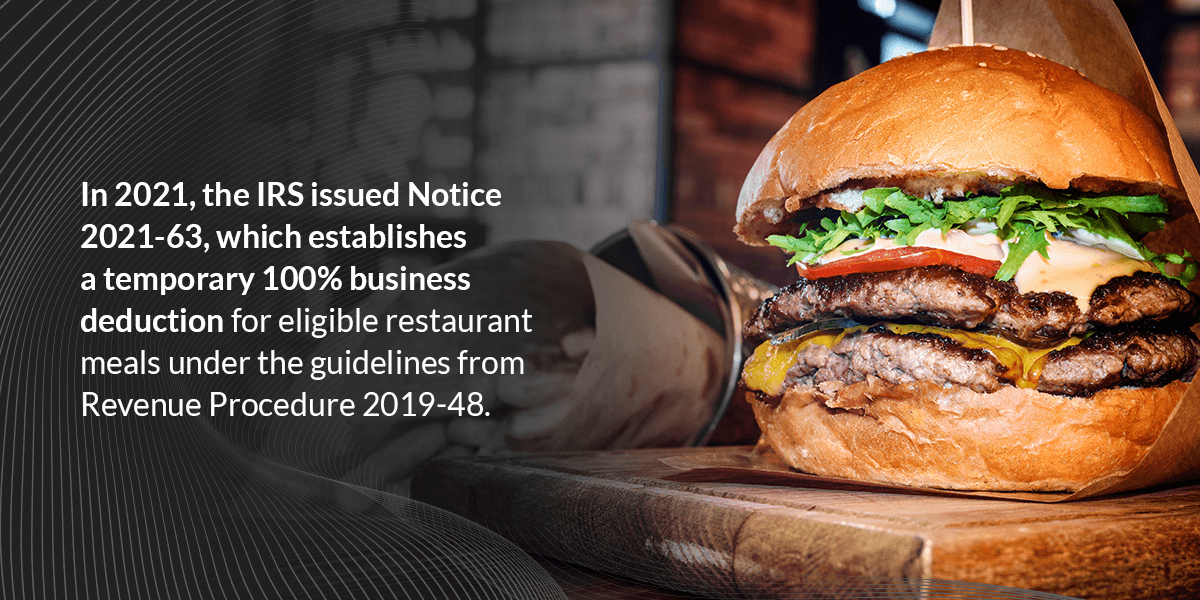

In 2021, the IRS issued Notice 2021-63, which establishes a temporary 100% business deduction for eligible restaurant meals under the guidelines from Revenue Procedure 2019-48. If you incur this expense during 2021 or 2022, you may qualify for this deduction for food and beverages from restaurants. This is a significant change from the 50% deduction limit as established by the Taxpayer Certainty and Disaster Relief Act of 2020.

What about non-restaurant meals? If you purchase a business meal with a client, this meal will still be 50% deductible unless you buy it from a restaurant. The same applies to office meals and snacks. For a company-wide party, the meal is fully deductible.

You can refer to Revenue Procedure 2019-48, section 6.05, to calculate the per diem rate for a meal. If you’re unsure how to determine the allowance incurred or paid or the per diem rate, discuss your tax situation with us at Polston Tax for assistance.

Changes were made regarding tax deductions for meals and entertainment under the Tax Cuts and Jobs Act. This act eliminated the deduction for entertainment, recreation or amusement expenses. Fortunately, you can continue deducting 50% of the cost of business meals under the following provisions:

According to IRS Notice 2018-76, “entertainment” doesn’t include activities that clearly do not constitute entertainment, even if the activities satisfy an individual’s living, family or personal needs, such as a vehicle or meals. These activities may be reimbursed by the employer or may include a hotel room the employer maintains for lodging employees during business travel. However, if a business provides a vehicle or hotel room to an employee while they’re on vacation, this would be considered entertainment of the employee.

For example, if you entertain clients in a luxury suite during a baseball game, you won’t be able to deduct the cost of the tickets or suite. Food included in the suite rental, provided to clients in the suite and not separated out, also won’t be considered tax-deductible. If your invoice does separate out the food costs, however, you can deduct it to the permitted extent. If you’re unsure about the tax deductions you can take this tax season, reach out to us at Polston Tax.

At Polston Tax, our professional tax resolution services deliver results. Our tax attorneys can help you resolve both state and federal tax issues, assist with audits and reduce or eliminate wage garnishments and liens. The following is our systematic approach to resolving tax issues:

We offer both tax resolutions services and tax and accounting services. Contact us at Polston Tax for tax help today.