Many individuals and businesses in the United States owe back taxes. Such taxpayers could face collection actions from the IRS, including levies. Levies allow the IRS to seize your assets to defray unpaid taxes. This mechanism is different from a lien, which is a legal claim against your properties to secure the payment of tax balance.

The IRS typically resorts to levies when they send several notices demanding the payment of taxes, but the taxpayer fails to respond or comply. If you receive a notice stating that the IRS intends to levy your properties, you must take proactive steps to find a resolution. Negotiating with the IRS at this point can be challenging — it’s best to work with an experienced tax professional.

The IRS sends LT11 notices when they intend to seize a taxpayer’s property or rights to property due to unpaid taxes. This is the agency’s last effort to collect back taxes before they begin levying your assets and property. When a person is sent LT-11, the IRS has made multiple attempts to collect and resolve a tax problem without resolution. The types of assets they can levy include:

You should contact the IRS immediately after receiving this notice to avoid a levy or other collection activities.

LT11 and Letter 1058 carry the same message, but LT11 is a shorter version. They both warn delinquent taxpayers that the IRS intends to levy their assets. The notices also inform the taxpayer about their right to a hearing. The deadline is usually 30 days, after which the IRS may file a notice of federal tax lien or levy your properties.

When you receive Letter 1058 from the IRS, they tell you it’s your last chance to rectify your back taxes before a levy occurs. You must read the notice and ensure you understand the content. Then, you follow the instructions. Ignoring the notice can result in adverse consequences. There are better ways to deal with such situations, even if you do not have the money to pay the amount in full. If you believe there is a mistake, you can request a hearing. The IRS needs you to communicate with them, or they will continue the collection efforts.

The LT11 letter is the last stop in the federal agency’s effort to collect back taxes. This also means they have likely given many other options and warnings to get the tax bill rectified but have not received a positive response. The IRS sends different notices depending on the situation. Here are four common examples:

One of the first communications you’ll receive from the IRS is the CP501 letter. This notice is the initial balance-due reminder. It informs you that you have unpaid taxes on one of your accounts. The IRS usually communicates in writing, so you’ll get this and all other notices in the mail to your last known address. The notice details your options, and you can go online for more information.

The CP502 letter is the second request for payment for the balance due on taxes. It’s sent when you fail to respond to the first reminder — the CP501 notice. The language in the CP502 is firmer because the IRS wants to convey the urgency in addressing past-due taxes. The letter will display the balance due with the applicable interest and penalties. That amount will likely be higher than the one you saw in the CP501 due to the additional interest and penalties, which will continue to increase until the bill is rectified.

The CP503 letter is the next in line to be sent if you don’t respond to the previous two requests. It’s the third notice about unpaid taxes from the IRS. Again, as time goes by without a resolution, the IRS will continue to tack on penalties and interest to the amount due.

If you’re getting this notice, you need to know the IRS is getting more intent on concluding. You have the same basic options with each of these letters. You can pay your bill or set up a payment arrangement with the IRS if you cannot pay the whole amount. It’s also worth noting that if you make the payment arrangements and don’t follow through, the IRS will quickly resume its collection efforts.

If you’ve ignored the previous three attempts, the next letter you’ll receive is the CP504. You will also likely notice that it takes a more serious tone than the previous attempts to get paid. The CP504 is the IRS telling you its intent to levy state tax refunds or other property. This letter provides a 30-day notice that if you don’t address the past due taxes, the IRS intends to levy your state’s taxes.

If you have any tax money from your state, the IRS intends to sieve it at the end of the 30 days. You have the same options—pay in full or establish a payment plan with the IRS to pay off your tax bill.

After sending several notices reminding and warning you about the unpaid taxes, the IRS will commence collection activities. Remember, the LT11 and Letter 1058 are final notices. They have already made at least four attempts to get you to respond. Now, they are ready to begin the levy process.

The IRS does not expect a response when sending the LT11 or Letter 1058 because they have sent numerous notices previously. However, they may give you one last chance to redeem yourself. If there is any leniency, the duration will likely be short. The primary intent is to levy, so you must be proactive. If you owe more than $62,000, the IRS can work with the State Department and revoke your passport too.

Considering the sensitivity of these situations, it would be best to work with experienced tax professionals. Tax professionals can review your case and help you respond. They can also negotiate with the IRS on your behalf to find a practical solution.

The IRS includes deadlines in the notices they send. The deadline for an LT11 notice is usually 30 days. You must pay the taxes you owe or respond within the period to avoid a levy. It’s not recommended that you wait until day 29 to respond. That may not give you enough time to work out an arrangement with the IRS or file for a hearing. Remember, once the IRS sends the LT11 notice, they are ready to levy. The challenge is that you won’t know what assets they plan to levy.

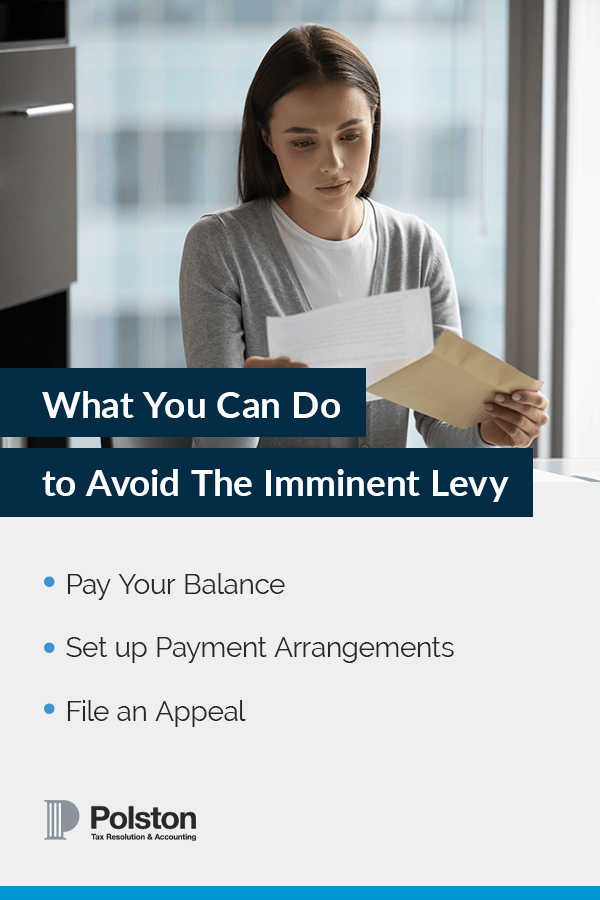

Since this letter is your last chance to respond, you might wonder what options you have. Your options have been outlined in each notice you’ve received. Let’s take a closer look at what you can do to avoid the imminent levy:

What the IRS wants you to do is to pay the amount you owe. You can pay the balance if you have the funds and agree with what is due. This will stop all collection initiatives, and the IRS won’t levy any of your assets as long as you have paid your balance in full. The LT11 and Letter 1058 provide directions for how to pay.

Many people don’t respond to notices from the IRS because they don’t have the money to pay the bill in question. If you don’t have the funds to pay your balance in full, you can contact the IRS to set up a payment arrangement.

Examples of the available payment options and solutions include:

You must follow through with the payment arrangements to prevent the IRS from resuming its collection efforts.

Another option you have, if you don’t agree with the amount the IRS says you owe, is to file an appeal. You should only file an appeal if you disagree with the amount owed. Don’t file an appeal just to avoid paying or getting a levy. You can use Form 12153 to request a Collection Due Process (CDP) or Equivalent Hearing. If, during your preparation for the hearing, you ascertain you do owe taxes, you can still attempt informal means to resolve the taxes due.

The IRS will levy your assets if you ignore the LT11 notice. You do not know which asset the levy will apply to. Also, remember that interest and penalties will still accrue. Your best option is to respond to the notice. You can consult with a tax professional if you need guidance on what to do.

A CDP hearing allows you to challenge the amount due if you believe the agency’s math is wrong. The hearing is usually the next step if you disagree with the LT11 or Letter 1058. You must request a CDP hearing within 30 days, or you can lose your rights. You will still be entitled to an equivalent hearing if you lose your right to a CDP hearing. You must request an equivalent hearing within one year.

The difference between CDP and equivalent hearings is that with CDP hearings, you can appeal further to the tax court if the Independent Office of Appeals rejects your claims. The option to appeal to the tax court is unavailable under equivalent hearings. The IRS Independent Office of Appeals conducts the CDP and equivalent hearings. Their primary aim is to attempt to resolve the dispute impartially without litigation.

There are several ways you can request a hearing. You can follow any of these options:

You will be asked to provide documentation to support your request for the hearing. You can continue to discuss your case with the collections department and negotiate up to the hearing. You can also appeal the outcome where the case would go to the US federal courts.

It’s best to contact a tax professional when you receive an LT11 or Letter 1058. Tax professionals can help in many ways, including the following:

We have an award-winning team with 100 years of combined tax resolution experience. This team comprises tax attorneys, accountants, financial analysts and enrolled agents, meaning you get end-to-end services at one destination. Our resources and capabilities have enabled us to serve individuals and businesses nationwide with an impressive success rate.

At Polston Tax, we pride ourselves on being a reliable and supportive tax consultancy agency. We are committed to forming lasting relationships with our customers and have done so for many years. We contribute to the community in different ways, extending our generosity to those who need help.

Our goal is simple — providing effective tax solutions regardless of case complexity. We explore all possible avenues and strive to implement strategies that suit our clients’ needs. We deliver results, and you can count on us to guide you throughout the process.

Getting an IRS notice of levy can be intimidating, but it’s often expected. It’s not the first notice you will receive if you have back taxes. LT11 or Letter 1058 is the final warning. If you fail to respond, the IRS will seize your assets to defray the tax balance.z Dealing with these notices alone can be challenging. Instead, reach out to a reliable tax professional.

Poslton Tax can help you navigate these difficult situations. We are ready to help. Contact us today to schedule a free consultation!