Paying taxes is an essential responsibility of every citizen, but in some cases, you may lack the funds to pay your taxes. If you face this stressful situation, you should know what to do. Failing to pay your taxes can have severe consequences, such as penalties, interest charges and even legal action.

To help, we’ll explore some of your tax options if you can’t pay your taxes. We’ll also discuss what happens if you pay your taxes late. At Polston Tax, we can help you find a resolution that works for you.

If you owe the IRS but can’t pay, act quickly. Ignoring the issue will only make things worse. The IRS can take legal action to collect your unpaid taxes, potentially resulting in penalties, interest charges, wage garnishment and even the seizure of assets. Here are some of the possible consequences of not paying your taxes.

To avoid these consequences, work to resolve your tax issue as soon as possible. You may have several available options, and when you reach out to us at Polston Tax, you can consult with a tax professional to determine the best course of action for your situation.

The IRS and many states offer options for people who struggle to pay their taxes. To take advantage of one of these this tax season, you must submit the correct paperwork and supporting documentation to the IRS.

A tax professional at Polston Tax can help you navigate the process that’s best for your situation. Alternatives if you can’t pay your taxes include the following.

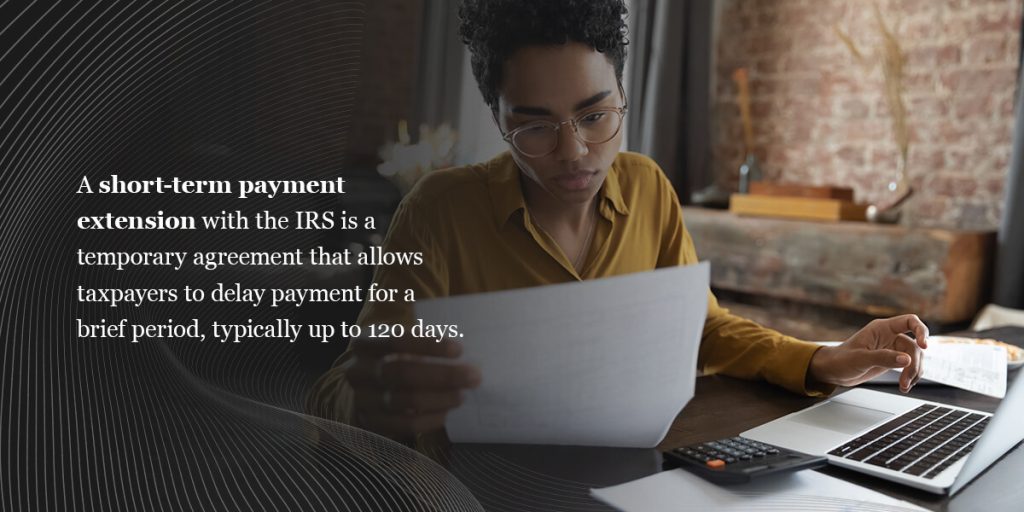

A short-term payment extension with the IRS is a temporary agreement that allows taxpayers to delay payment for a brief period, typically up to 120 days. This option is available to taxpayers who cannot pay their tax bill by the due date and need a little extra time to come up with the funds.

To request a short-term payment extension, you may need to contact the IRS and explain your situation. The agency may ask for some financial information to determine whether you are eligible for this type of relief. If they approve your extension, the IRS will give you additional time to pay your taxes, but interest and penalties will still accrue on your unpaid balance.

A short-term extension is not a payment plan and does not provide long-term relief from a tax balance. If you cannot pay your taxes within the 120-day extension period, you may need to explore other avenues, such as a payment plan or an offer in compromise. Additionally, you must file tax returns on time to avoid additional penalties and interest charges.

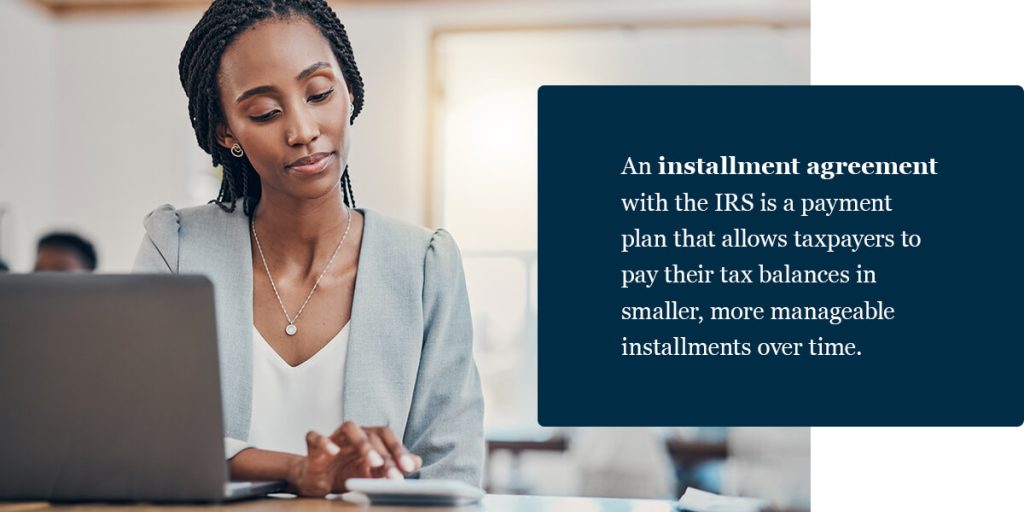

An installment agreement with the IRS is a payment plan that allows taxpayers to pay their tax balances in smaller, more manageable installments over time. This option is available to taxpayers who can’t pay their tax bill in full at the time of filing. The IRS offers several types of installment agreements.

To apply for an installment agreement, you should submit Form 9465 to the IRS. The form requests information about your financial situation and proposes a monthly payment amount based on your ability to pay. If approved, you must make monthly payments until you pay off your tax balance in full, including any interest and penalties.

Interest and penalties may continue to accrue on any unpaid balance until you pay your taxes. Additionally, you must continue to file tax returns on time and pay any taxes owed in the future while on an installment agreement. If you are unsure whether you qualify for an installment agreement, reach out to us at Polston Tax today.

A guaranteed installment agreement is an arrangement with the IRS that allows taxpayers who owe $10,000 or less to pay their tax balance in monthly installments for up to three years. This type of agreement is “guaranteed” because the IRS must accept your request if you meet the following criteria.

If you fulfill these requirements, you can apply by submitting Form 9465 to the IRS, providing information about your income, expenses and assets. This form also proposes a monthly payment amount based on your ability to pay.

If approved, you must make monthly payments until you pay your tax balance in full, including any interest and penalties that may accrue. The IRS may still file a federal tax lien on your property, though it may be possible to have the lien released under some circumstances.

A financially verified installment agreement is another IRS payment plan that gives taxpayers more time to pay their back taxes. This arrangement requires you to provide detailed financial information to the IRS to verify your ability to pay.

To apply for a financially verified installment agreement, you must submit Form 433-F to the IRS. This form requests information about your income, expenses, assets and liabilities. The IRS will use this information to determine your ability to pay and calculate a monthly payment amount.

Once the payment plan is in place, you must make monthly payments until you pay your tax balance in full, including any interest and penalties that may accrue. The IRS may periodically adjust your payment amount if your financial situation changes.

Note that if you choose to apply for a financially verified installment agreement, you may need to provide additional documentation to the IRS, such as proof of income or expenses.

An offer in compromise is an agreement between a taxpayer and the IRS to settle a tax balance for less than the total amount owed. The IRS may accept an OIC if you cannot afford to pay the full tax liability and accepting the offer proves to be in the government’s best interest.

To apply for an OIC, you must submit Form 656 to the IRS. The form requests detailed financial information about your income, expenses and assets. You must also propose an offer amount that you believe is a reasonable compromise based on your ability to pay.

The IRS will evaluate your offer based on several factors, including your income and expenses, your ability to pay, the value of your assets and any unique circumstances that may justify accepting a lower amount. If the IRS accepts the offer, you must pay the agreed-upon amount within a given time.

Not all taxpayers can qualify for an OIC, and the process can be lengthy and complex. Additionally, submitting an OIC does not stop interest and penalties from accruing on the tax balance.

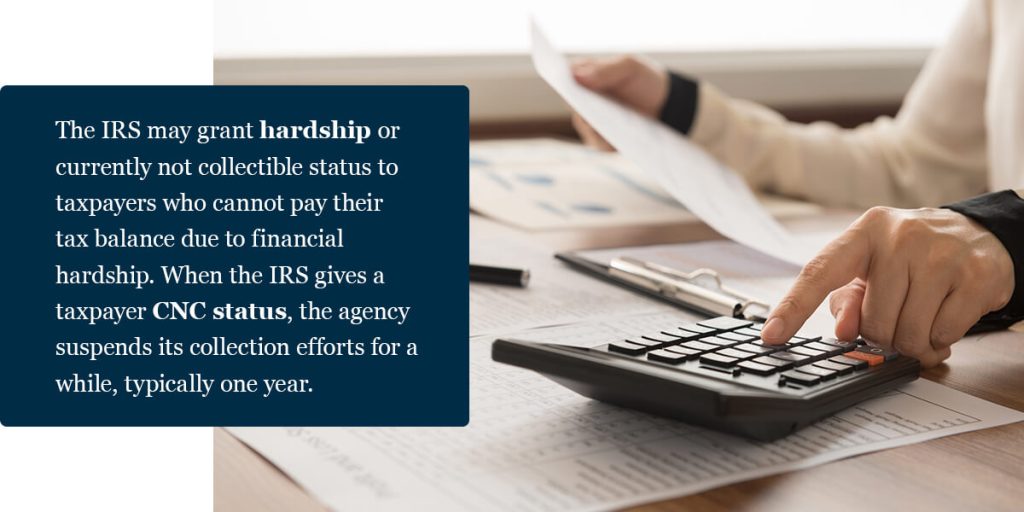

The IRS may grant hardship or currently not collectible status to taxpayers who cannot pay their tax balance due to financial hardship. When the IRS gives a taxpayer CNC status, the agency suspends its collection efforts for a while, typically one year. During this time, you may not need to make payments on your tax balance, and the IRS will not take any collection action, such as asset seizure or wage garnishment.

To qualify for hardship or CNC status, you must demonstrate to the IRS that paying the unpaid taxes would cause undue financial hardship. Proof may involve detailed financial information, such as income, expenses and assets. The IRS will evaluate your financial situation to determine your eligibililty for CNC status.

While CNC status can temporarily pause collection efforts, it does not cancel the tax bill. Interest and penalties will continue to accrue on the balance while it is in CNC status. Additionally, the IRS may periodically review your financial situation to determine whether you are still eligible for the status.

At Polston Tax, we can help you determine whether you may be eligible for CNC status and apply for tax relief.

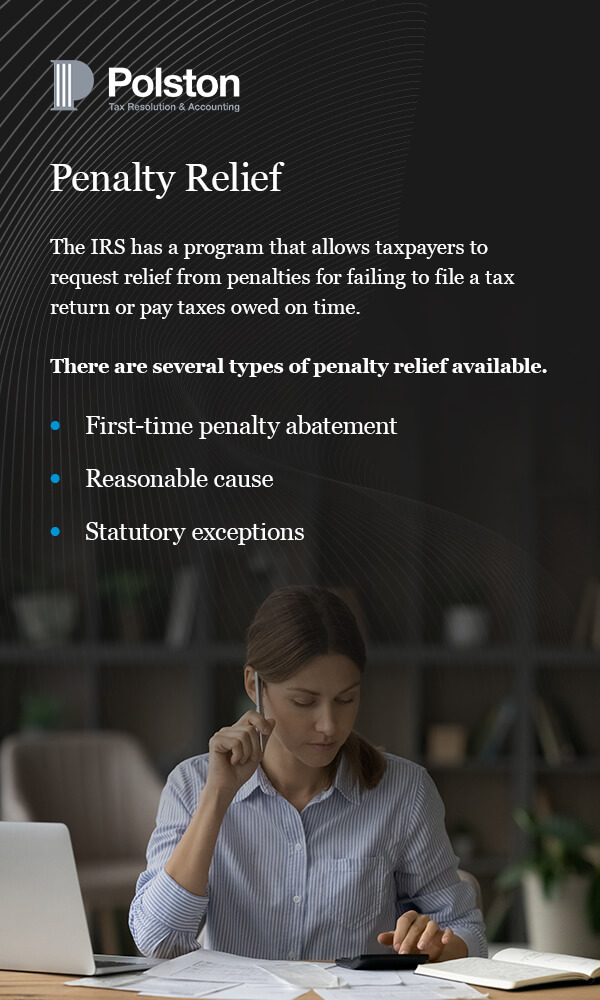

The IRS has a program that allows taxpayers to request relief from penalties for failing to file a tax return or pay taxes owed on time. The IRS may grant penalty relief in qualifying circumstances if you have a valid reason for failing to file or pay on time, such as a severe illness or natural disaster.

There are several types of penalty relief available.

To request penalty relief, you must submit a written request to the IRS explaining your reason for requesting relief and providing any supporting documentation. The IRS will evaluate your request and make a determination based on your circumstances.

Penalty relief does not cancel the underlying taxes owed. If the IRS grants you penalty relief, you may still be responsible for paying any taxes owed, including interest and other penalties that may continue to accrue on the balance.

If you owe taxes you cannot pay, consult with a tax professional at Polston Tax for assistance.

Every situation is unique, and we can help you find the right solution for your financial needs. The IRS provides multiple options for paying down taxes owed.

Other alternatives may work for you too. A tax professional from Polston Tax can evaluate your situation, status and ability to pay. We can help you make the right decisions for paying off or reducing your tax balance.

During the work year, you may need to make estimated tax payments to the IRS. These may be through automatic withholding for W-2 employees or manual payments from contractors, freelancers and self-employed people.

When you file your tax return, you get a refund if you paid more income tax than necessary. If your estimated payments fall short, you will owe the IRS money.

If you owe taxes and don’t pay on time, you’ll receive a notice from the IRS. You’ll receive at least one more notification if you don’t pay at this point.

During this time, any unpaid taxes will begin accruing interest and penalties. Interest starts accruing according to the due date on the notice. It compounds daily to the unpaid tax balance.

There are additional fees as well. The failure-to-pay penalty is 0.5% per month, up to the maximum of 25% of your unpaid balance. You will also owe additional interest and penalties on any unpaid local or state taxes, according to rates set by your state.

At this point, any unpaid balance may come out of your future tax refunds. Beyond this, the IRS could place a lien on your assets or property. A lien could later become a levy, which means the IRS could seize your property for payment on your tax bill.

If many years have passed, time may be on your side. There’s a 10-year statute of limitations for collecting late taxes. If you are concerned about the penalties or taxes you may face on unpaid taxes, contact us at Polston Tax today.

Paying taxes is a challenge for many people. However, if you neglect your taxes year after year, the tax burden continues to pile up. If you haven’t paid taxes in multiple years, we recommend addressing the situation as soon as possible. Otherwise, you could face severe consequences.

The IRS can collect late taxes for up to 10 years. There are a few exceptions for bankruptcy, living abroad or filing an offer in compromise or an installment agreement.

Here are a few steps to take if you owe a lot of back taxes.

The IRS keeps tax transcripts for each year you’ve worked and earned income if your employer reported it. You can request a transcript from the IRS to determine what they believe you owe in taxes.

There are five types of transcripts.

If you are planning to file taxes for prior years, collect as much documentation as possible, including 1099 and W-2 forms. You may need to contact previous employers who may still have this information on file.

Finding previous tax return forms is simple. The IRS has a database that goes back over a century. It’s in your best interest to contact a tax professional at Polston Tax to ensure you are filing back taxes correctly.

You want to be sure you’re taking the correct exemptions and deductions for each year you need to file back taxes. If your tax balance is too high, the IRS has options to help you.

If you owe more than you can afford to pay, don’t ignore the problem. Contact the IRS to set up a payment plan or another alternative. If you would rather not reach out to the IRS on your own, you can turn to us at Polston Tax. We can handle communications and negotiations with the IRS on your behalf.

There is no one-time tax forgiveness program that applies to all taxpayers. However, in some circumstances, the IRS may offer relief to taxpayers who cannot pay their taxes due to financial hardship or other extenuating circumstances.

One example is the IRS Fresh Start Program, established to help taxpayers who struggle with unpaid taxes. If you are eligible for this program, you may be able to set up a payment plan, request a temporary delay in collection or negotiate a settlement with the IRS. The program has different requirements and eligibility criteria depending on the specific situation, so consult with a tax professional at Polston Tax to determine if you qualify for relief under this program.

Another option is to request an OIC, which is an agreement between you and the IRS to settle the tax balance for less than the total amount owed. However, the IRS generally only grants OICs if you cannot pay in full and have no other means of resolving the tax balance.

Even if the IRS grants you relief under one of these programs, you must still file your tax returns and pay any taxes owed in the future. Additionally, interest and penalties may still accrue on any unpaid taxes.

If you’re struggling to pay your taxes or are facing years of unpaid taxes, there is hope. It’s a common problem, and options are available to help you pay your tax balance and get back on track.

At Polston Tax, we tackle your tax problem for you! You will have a whole team of tax professionals on your side. Our goal is to provide the tax help you need to resolve your tax liability issues once and for all.

We’d love to hear from you and help you with all your tax needs. Contact Polston Tax today to get started.