Summary: This article provides a guide to understanding capital expenditures. Capital expenditures are investments in long-term assets, such as property, equipment, and buildings, that are expected to benefit a business for more than one year. This article explains that capital expenditures are not fully deductible in the year they are incurred; instead, they are depreciated over the asset’s useful life. It highlights the importance of properly classifying expenditures as either capital expenditures or ordinary business expenses for accurate tax reporting. Understanding capital expenditures is crucial for businesses to manage their taxes and make informed investment decisions.

It’s almost impossible for a business to survive and thrive without capital expenditures. However, these costs can also skyrocket, making a huge hole in a business’s pocket. Tax deductions can provide a way for businesses to recover some of the costs. However, assets considered capital expenditures are not always tax-deductible right away.

This article breaks down what makes capital expenditures different from other expenses. You’ll also learn how they work, how they can be tax-deductible and what alternative methods can help you recover the costs.

Capital expenditures (CapEx) are business funds you use to purchase qualified assets aiming to improve business operations, such as equipment or vehicles. CapEx assets are considered investments, so they’re not treated as traditional business expenses that imply money is leaving the business. Rather, the money took on a different form, which increased the company’s profitability. Aside from acquisitions, CapEx includes funds used for repair, improvement and maintenance of the assets with certain conditions.

Because capital expenditure is not an expense for tax purposes, they cannot receive full tax deductions in the first year, with a few exceptions. Qualified assets benefit the business beyond one tax year. For example, if business equipment can last five to eight years, you spread the deductions throughout its lifetime. This is known as capitalization, depreciation or amortization.

Since you can stretch their usefulness over a span of years, it’s not accurate to deduct the full cost of a CapEx asset only in its first year. Instead, calculating deductions involves the depreciated value.

By definition, capital expenditures lose their value over time. You cannot consider business expenses that only have a one-year lifespan or less as capital expenditures. These business expenses are considered operating expenses (OpEx) and are tax-deductible in the year you purchased them. Office supplies, payroll and insurance costs are some of what fall in this category.

However, some capital expenditures qualify for full deduction under Section 179 of the Internal Revenue Code (IRC). These assets can have full deductions in the first year you use them, though not necessarily the year you acquired them. We discuss Section 179 more below.

Capital expenditures are usually tangible assets that you can depreciate. However, some intangible assets may qualify. You must use these assets for business purposes or income-producing activities, and they must have a life expectancy of more than a year. This life expectancy should be determinable and not vague. You cannot capitalize or depreciate land because land does not become obsolete or wear out.

Tangible business assets include:

Intangible business assets include:

The depreciation of CapEx is part of your annual income tax deduction. It helps you recover the costs of your assets, considering their diminishing value until they become obsolete. Note that depreciation only starts the year you use the asset, regardless of when you purchased it. For example, if you purchased equipment in December 2024 but didn’t use it until January 2025, the depreciation starts in January 2025.

Also, you don’t need to stop depreciating the asset even if you’ve stopped using it temporarily. You only stop depreciating at the end of its life cycle or once you fully recover the cost. Say you use one machine to produce a seasonal product. You can continue to depreciate the machinery even when you aren’t using it to make the product.

However, you need to be aware of depreciation recapture if you plan to sell. Depreciation recapture enables the Internal Revenue Service (IRS) to tax you if you sell a qualified asset for more than its depreciated value. For example, if equipment is valued at $15,000 due to depreciation but you sell it for $25,000, the IRS will tax the $10,000 difference.

Depreciation for CapEx is technically an accounting procedure. The IRS requires using the Modified Accelerated Cost Recovery System (MACRS) of depreciation for properties used after 1986. Based on MACRS, accountants can use one of two methods when calculating the depreciation amount. The IRS specifies the number of years to depreciate an asset based on the mode of depreciation.

The two methods of depreciation for MACRS are:

Some intangible assets, like books, sound recordings, motion picture films, copyrights and patents, can use the income forecast method as an alternative depreciation method due to uneven revenue.

Some of the GDS recovery periods are:

Some of the ADS recovery periods are:

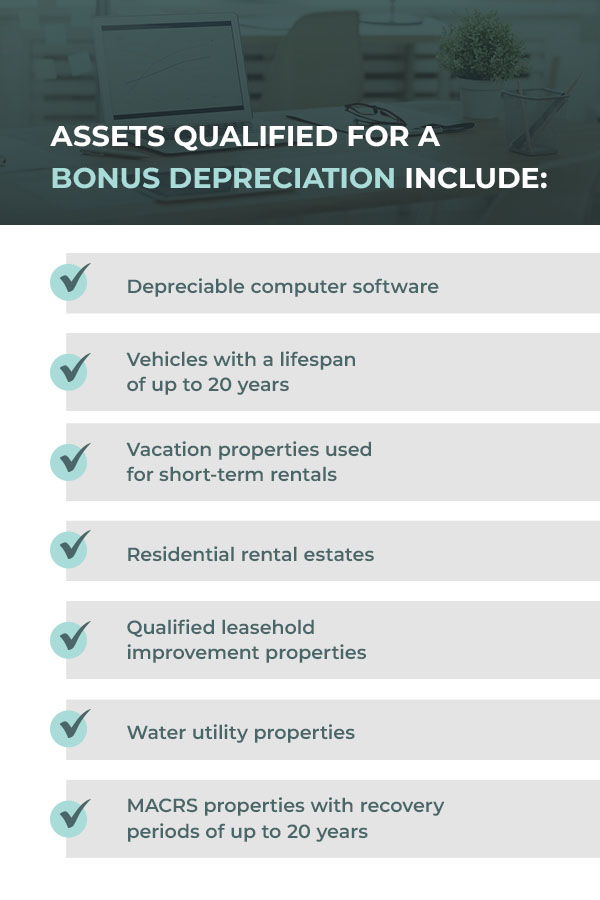

Bonus depreciation, also known as the special depreciation allowance or additional first-year depreciation, helps you recover parts of the cost for your qualified assets. It lets you deduct a large amount in the first year and spread the rest of the cost throughout an asset’s lifetime. This tax incentive can be added on top of any Section 179 deduction.

The Tax Cuts and Jobs Act (TCJA) temporarily allowed 100% depreciation allowances for assets used from September 27, 2017, to January 1, 2023. The 100% allowance decreases by 20% yearly starting in 2022, which made the 2025 bonus depreciation 40%. It will be 20% for 2026, and the bonus depreciation phases out by January 1, 2027. You need to report any bonus depreciation to the IRS.

Some assets qualified for a bonus depreciation include:

Safe harbor election allows you to deduct certain amounts for tangible properties instead of capitalizing them. For instance, repairs and improvements generally qualify as capital expenditure. But with a safe harbor election, you can choose to deduct expenses instead. These can involve improving and restoring a property or adapting the property to a different purpose. Some expenses do not qualify for a de minimis safe harbor, such as inventory, land, and certain emergency and spare parts.

The threshold per invoice ranges from $500 to $2,500 without an applicable financial statement. The limit increases to $5,000 per invoice if you have one. Note that the de minimis safe harbor election does not require your business to capitalize any excess cost from these thresholds. The typical rules will apply for this excess.

For small taxpayers, these are the requirements for the safe harbor election:

Routine maintenance qualifies for deductions in the following cases:

Unlike other capital expenditures, assets that qualify under Section 179 of the IRC can be fully tax-deductible in the first year. The deduction is generally the cost of the asset, assuming the price is not over the tax deduction limit. For 2025, the cap is at $1,250,000. Sports utility vehicles are capped at $31,300. The IRS can adjust these values yearly.

Also, the Section 179 phase-out threshold for 2025 is at $3,130,000. You cannot receive a 100% deduction for purchases costing more than this amount. If the cost is greater than this threshold, you’ll be limited to bonus depreciation, which has a much lower deduction rate of 40% in 2025.

Additionally, you cannot have deductions more than your taxable income for the year. However, you can deduct any excess in the following year. For example, say your income is $150,000 and the deduction amount is $200,000. You can only deduct up to $150,000 for that year, but you can deduct the remaining $50,000 the next year.

Tax-deductible capital expenditures include tangible business properties. Computer software is also generally qualified. If the property is only partially used for business purposes, more than 50% of the property should be used for business. Investment and rental properties and properties that produce royalties do not qualify. Qualified tangible properties can include those of the following industries:

In general, Section 179 aims to encourage companies to invest in themselves and acquire assets that enable them to do so. It can be especially beneficial for smaller businesses as the tax deduction provides huge tax relief.

Operating expenses or current expenses are another type of business expense. These are defined as ordinary and necessary business expenses. Unlike CapEx, OpEx doesn’t have a life cycle of more than a year. Examples include your monthly rent or electricity bills, where you “use up” the paid amounts in a month. These are tax-deductible in the year you incur them.

Repairs and improvements can be considered an operating expense if they are simple and incur minimal costs, so you may wonder if expensing capital expenditures is a better option. It might not make sense to capitalize if, for instance, your repair costs fall within the threshold of the safe harbor election.

If you’re unsure whether capitalizing vs. expensing costs are ideal for your business, here’s a quick direct comparison:

| Capitalizing Costs | Expensing Costs |

|---|---|

| You record expenses on a balance sheet. | You record expenses in an income statement. |

| The purchases are treated as an investment. | The purchases are treated as ordinary but necessary. |

| It can showcase higher profits, making you owe higher taxes. | It can showcase lower profits, so you can owe lower taxes. |

When deciding, consider factors such as an asset’s life cycle. Remember that if you capitalize an asset, you may be able to apply multiple deductions depending on the asset’s qualifications. For instance, purchasing equipment can qualify for a Section 179 deduction, a bonus depreciation deduction and a standard first-year depreciation under MACRS. Capitalizing an asset can lead to huge savings, but this might not be necessary if the costs are too small.

Taxes can be tricky to navigate with all of the rules and requirements set by the IRS. Capital expenditures are no exception. You need to consider an asset’s life cycle, qualifications, depreciation rates and deduction limits. The good news is that you don’t have to do it all by yourself. Whether you’re a small business or an enterprise, Polston Tax can help you out.

We can prepare your tax returns for you and help you solve tax-related problems you might not have time for. Our team consists of tax attorneys, case managers, accountants and tax preparers, so you can count on our extensive knowledge of the tax code and tax laws. You can contact us today to get started! We offer free consultations.