Summary: This article discusses tax planning strategies for farmers, focusing on how to qualify for certain exemptions. It highlights unique tax rules applicable to farmers, such as the ability to average farm income over multiple years. This article emphasizes the importance of keeping accurate records of income and expenses. It also suggests exploring deductions and credits specific to the agricultural industry. Proactive tax planning is crucial for farmers to minimize their tax liabilities and maximize their profitability.

If you’re a farmer or agricultural business owner, you face some unique tax situations. Proper tax planning strategies can improve your financial management and maximize profitability. Learn about different kinds of tax exemptions available for farmers, how to become a tax-exempt farm and common mistakes to avoid.

Several tax exemptions are available to farmers and ranchers. These exemptions can reduce your taxable income or your tax liability. There are state and federal exemptions.

The broadest ag exemption is state sales tax. Many states offer sales tax exemptions on items used directly in agricultural production. Here are some of the products that often qualify:

Some states require showing a tax-exempt permit card when purchasing supplies or personal property for agricultural activities. Some permits have exclusions, such as on vehicle purchases.

Federally, Section 179 of the tax code allows farms and ranches to deduct business expenses for depreciable assets such as equipment and vehicles. This deduction lowers the taxes due for the year when the equipment was purchased rather than depreciating it over time. This exemption is only for expenses deemed ordinary and necessary for running a business. Though mainly used for equipment, it can also cover tangible personal property, such as livestock, software, testing equipment, and single-purpose agricultural or horticultural structures, such as livestock shelters.

For the 2024 tax year, the expense deduction limits increase to $1,220,000.

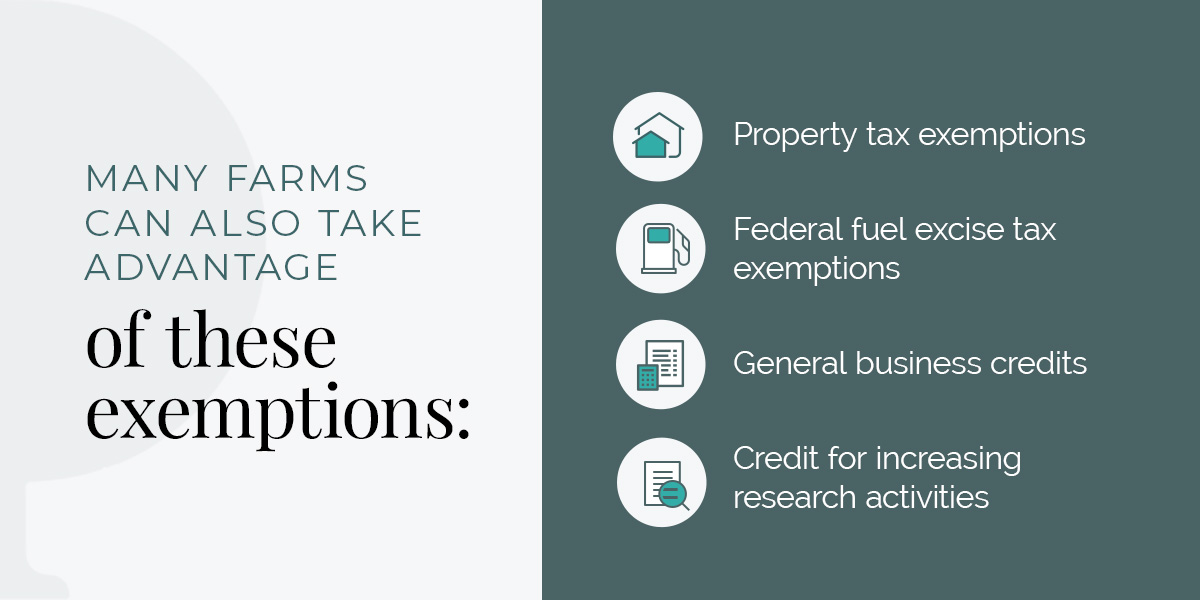

Many farms can also take advantage of these exemptions:

To become a tax-exempt farm, you must apply for special permits or submit certain forms to your local taxing entity or the IRS.

State laws vary and may include minimum property size or dollar amount for agricultural sales. In some states, leasing your land to a farmer or rancher is enough to qualify for property tax exemptions. However, depending on zoning laws or other property restrictions, you may not be able to sell agricultural products from a residential property even if you have a business permit.

In many states, farmers must apply for a tax-exempt permit to avoid paying sales tax on purchases for their business. For example, to qualify for an Oklahoma farm tax exemption, farmers or ranchers can apply for an agricultural exemption card from the Oklahoma Tax Commission (OTC) using the Oklahoma Taxpayer Access Point (OkTAP), the state’s online payment system. Farmers must submit relevant IRS forms and other documentation demonstrating farming or ranching for a profit and renew every three years.

First, ensure your operation is legally a farm as defined by the IRS. Generally, a farming business raises or grows a product and sells that product without further processing or modification. Examples of qualifying farm activities include:

Revenue from being open to the public, such as entry fees or donations to help run an educational program, can still count if those activities are directed toward improving marketing or other business conditions rather than just improving production or conditions for workers. However, running something like a “dude ranch” or a resort, even on farmland, wouldn’t count.

Federally, there is no minimum acreage for farm tax. Instead, the IRS is concerned with whether you operate your farm like a business, how you intend to make a profit and how much you depend on farm income for your livelihood. If less than two-thirds of your income is from farming, you may still qualify if you can prove a profit motive.

Which forms and schedules you’ll need to fill out depends on the type of business you run and which exemptions or credits you claim.

Here are some of the most common mistakes farmers make regarding ag tax exemptions:

When you’re ready to invest in tax consulting, trust Polston Tax Resolution & Accounting. We’ll put together the perfect team for your business, which can include an accountant, a tax preparer, a tax attorney and a case manager. When you work with Polston Tax, you get advice from experienced professionals who understand what it takes to run a successful farm and keep up with changing laws. We offer many services to support farmers and ranchers in streamlining their operations and achieving long-term success.

Reach out online today to find out how Polston Tax can help your farm.